Emerging KYC Methods

Countering financial crime is one of the main security issues in the banking sector at the moment. Most of the requirements are determined not by the internal policy of the bank, but by the legislation of the national or international level. Failure to comply with the requirements of the bank leads to large fines and a blow to the company's image. To prevent incidents, modern banks form a customer relationship policy based on Know your customer (KYC) principles.

Most banks, investment and financial companies invest in the development of new KYC solutions and actively cooperate with FinTech startups. Let's consider the emergence of which identification methods such cooperation has led to.

In a growing economy, financial companies can be vulnerable to criminal activity. And along with the provision of services, FIs are required to comply with the regulations, protecting the finances and data of their customers from fraud.

While in the case of trade in goods and services, risk insurance is carried out under the terms of the contract, in the case of financial systems, the instruments themselves must include security measures in which companies invest heavily. There is no single standard for what these measures should be; they usually differ depending on the financial services company responsible for establishing its effective security policy. However, government agencies involved in combating financial crimes, issue and monitor compliance with certain regulations. One such regulation is Know Your Customer (KYC), which was introduced in the 2000s by FinCEN, a bureau of the U.S. Department of the Treasury.

KYC is a method carried out by companies, most often banks, to verify the identity of their client in accordance with the requirements of legislation and anti-money laundering regulations.

KYC includes:

personal identification;

understanding the nature of the client's activities, and the origin of finance;

assessment of risks associated with possible money laundering.

In an era of rapid technological development, the requirements for KYC are intensifying. Stricter financial crime regulations are forcing banks to spend more resources and time on security solutions. And while resources are a pain point for financial companies, time and inconvenience is a concern for many clients, for whom going through the identification process can be annoying and burdensome.

Initially, the identification process took a lot of time, as a client had to provide documents and confirm their identity at the bank branch in-personally. This manual process was extremely inconvenient and did not contribute to a better customer experience at all.

Fortunately, with the development of technology and the advent of the pandemic, neobanks and fintech companies have switched to digital identity options, automating their processes. This had a positive impact on the improvement of the financial services, since clients do not waste time travelling to a bank office, but provides data remotely via secure channels. Although implementing seamless digital onboarding solutions can be quite costly, it has its own rewards.

So, as we have already found out, the KYC procedure is to verify that a client is really who they claim to be and provide access to the services they need. This verification may take place in various ways, the choice of which is left to the FIs.

Since lengthy questionnaires and complicated checks can turn off the bulk of potential customers, the challenge for financial services companies is to simplify identification methods while maintaining reliability and complying with high standards and current regulations.

The electronic version of identification, called eKYC, uses photo or video identification, significantly saving the time for the client to receive the desired services. The best modern practice for connecting a client to bank services, called onboarding, is considered to be multi-level KYC. This is a flexible approach in which the user verification procedure is determined by the requested service. For example, a user who simply wants to get to know financial products and services will not be required to go through a full KYC process. While obtaining a loan or making relatively large transactions will most likely require the provision of additional pieces of verification documents.

Such not 1-for-all approach contributes to creating an outstanding user verification experience that also includes the following key components:

Multi-level Onboarding.

This flexible approach allows new clients who want to explore available financial services to avoid identity verification. At the same time, in order to receive a needed financial service, such verification will be mandatory.

Balanced KYC Compliance.

To meet the requirements for combating financial crime on the one hand, and on the other hand to provide an excellent customer experience, financial companies should maintain a happy medium in the choice of procedures and risk policies.

Of Benefit to Customers.

KYC compliance benefits not only FIs that protect themselves from the risks associated with financial activities, but also customers who are confident that no one but them will have access to their personal information or funds.

The development of financial and banking technologies has led to the emergence of new effective KYC methods. Let's take a look at 5 of the most common.

Prior to the introduction of certain digital solutions, KYC compliance required an in-person verification (IPC), i.e. a face-to-face meeting between the client and a bank representative and submission of necessary documents. This procedure is still used in some countries and companies to provide certain financial services. But now this practice is used less and less, as banking systems introduce technologies such as streaming video, allowing to confirm identities remotely through video verification.

Also, with the secure file sharing feature, customers do not need to bring their documents in person or deliver them by courier, as more and more companies adopt a paperless approach, accepting ID, proof of residence and other required documents in digital form.

The manual KYC process has been digitalized and transformed into eKYC, allowing companies that have been open to technological advances to move the identity verification process online. Technologies such as artificial intelligence (AI) and machine learning (ML) used by FinTech have made a breakthrough in creating new innovative ways to comply with KYC.

So, for example, to check documents and photos sent electronically, corporate-level software uses Optical Character Recognition (OCR) and ML algorithms. In this way, companies can be sure that the documents that were obtained for identity verification are genuine and belong to their client. For this matter Neofin offers its own built-in Liveness detection and face recognition tool that will help you to prevent fraud in early stages.

Automated eKYC/AML verification is superior to manual verification in many ways as it eliminates human errors, improves customer experience, and reduces costs.

The open banking model has been a big win for banks and other financial services companies, as it has allowed them to integrate third-party providers into their product portfolio via APIs and offer value-added services to customers. Banks can also analyse data obtained from third-party services used by customers to better understand their needs, as well as conduct proper underwriting and AML / KYC checks.

With access to data from various sources, FinTech companies no longer need to collect and interpret data from scratch. Thus, verifying the identity of customers has become easier, safer, and more cost-effective.

Customers also benefit from KYC-enabled open banking, accessing banking services with a single click, without having to go through lengthy in-person or eKYC verification processes.

Neofin has off-the-shelve integration with popular open banking and income verification services like Plaid, Argyle, Dapi, Highline and others. Here you can find the list of all available integrations.

4. Phone Identity Verification

Mobile phones can tell a lot about their owners, which is why they are also widely used for identity verification. Mobile identity technology greatly simplifies KYC verification, which automatically improves the onboarding process.

What's more, mobile phone verification is accurate. All received data related to the behaviour of the phone, including calls, SMS, the frequency of changing SIM cards or phone line, and even the contact list, is monitored and analysed to determine whether the client is involved in suspicious transactions.

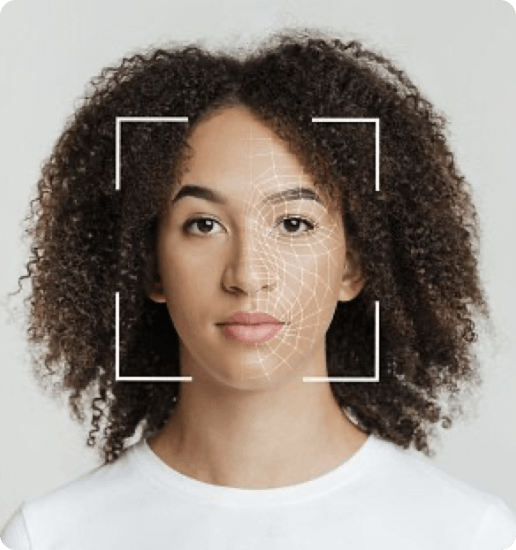

NFC-enabled phones with biometric sensors have become another solution for identity verification. The advantages of this method are its availability and efficiency. To access financial services, customers need only have a device that supports biometric sensors. Customers can either scan their eye or fingerprint or use the recognition function to verify their identity and access their account or use their bank's products.

An integral part of the biometric authentication system is the liveness detection technology, which is used in modules by Neofin. With its help, the system determines whether it is interacting with a “real” person or a fraudster using a fake ID: a face photo, video, realistic mask or deepfake.

Authentication and identification of users have become a stumbling block for a large number of financial services. On the one hand, fintech companies strive to provide customers with seamless authentication in a service or application. On the other hand, simplifying this procedure may lead to a security breach, and this should not be allowed.

Modern technologies make it possible to use KYC methods that were previously unattainable. First of all, these are biometric methods, when a computer system recognizes a person by face, retinal pattern, voice or fingerprint.

Of course, this is not the end of the development of this important aspect of the financial industry, and more and more KYC solutions are ahead of us, which will further contribute to creating a better user experience and more personalised offers.